The Changing World of OCC

the bottom line| OCC MARKETS

The Changing World of OCC

ILKKA KUUSISTO

Old corrugated containers (OCC) are the main fiber raw material for corrugating materials, brown boxes used mainly for transport packaging. This market is growing globally, but it is also changing. This article looks at some of these changes and what they mean to the paper industry.

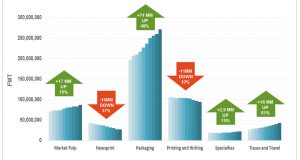

For the past two decades, the world has been dividing into two parts: the rapidly growing “emerging markets” of mainly Asian countries; and the stagnant, or slow-growing “Western countries,” which include North America, Western Europe, and Japan. Now these Asian emerging markets have become the leading paper-consuming region, with half the global paper production and the lion’s share of global investment (Fig. 1). But they remain short on fiber even more than before. To feed all these new paper machines, Asia has been importing increasing volumes of fiber in all forms—round logs, wood chips, pulp, and recovered paper. This endless appetite for fiber has changed the market forever. Now this market is about to change again.

CHINA THE DYNAMO

China is the key to this development, being the new economic dynamo of Asia as well as the largest producer and con-sumer of paper, paperboard, and all packaging materials worldwide. China is also the largest importer of recovered paper, including OCC.

China’s economic growth is slowing; it has been for a few years, and there has been a lot of speculation about whether it willbe a hard or soft landing. In fact, it is not going to be a landing at all, just a slower overall growth, which is natural when an economy gets to be as big as China has become. But slow growth in a big economy still means a lot more tons every year than a much higher growth from a small base.

At the same time, the Chinese economy is changing. What used to be an investment-driven manufacturing center for the world is now increasingly becoming a more domestic oriented consumer society. Industrial development is moving away from the coastal areas, both to inland provinces (where the growth will continue, albeit at a slower pace than in the export boom of the past 15-20 years) and outside of China to places like Vietnam and other nearby countries with large populations and low income levels.

This structural change affects the Chinese packaging market in many ways. The slower economic growth will eventually mean less investment in new paper machines, though there will continue to be new investments located in inland provinces. Some of these are smaller machines, which can be simpler and cheaper as they target local consumers for local box manufacturing. In such instances, quality requirements will be easier to meet. Shorter transport distances reduce damage so the boxes don’t need to be as strong and there will be less extreme variations in weather conditions, etc.

However, many big and modern machines are still in the pipeline, including those for the inland provinces. This domestic, inland focus will also mean that more corrugated boxes will remain in China and, increasingly, in inland provinces. There they can be collected locally and used as raw material by the local paper mills. Less developed countries and regions tend to have a higher proportion of other uses for old boxes—whether for re-use, for other packaging, or even as floor coverings. This tends to decrease when a nearby mill can create a market for the material.

In Asia, waste paper is not waste, but a valuable commodity that has a price at the point of collection. Use of recycled boxes close to their origin means that  the rate of circulation will be faster: The cycle from re-pulping OCC at the mill toproducing liner and medium, to making boxes and using them, and eventually collecting the OCC and bringing it back to the mill will be significantly faster when the whole cycle happens within a few-hundred-kilometer radius. The long cycle of export manufacturing, product exports to the US or Europe (Fig. 2), and eventual collection and return freight will be avoided. This not only reduces costs, but the same boxes can be recycled more than once in a single year, reducing nominal yearly consumption of OCC.

the rate of circulation will be faster: The cycle from re-pulping OCC at the mill toproducing liner and medium, to making boxes and using them, and eventually collecting the OCC and bringing it back to the mill will be significantly faster when the whole cycle happens within a few-hundred-kilometer radius. The long cycle of export manufacturing, product exports to the US or Europe (Fig. 2), and eventual collection and return freight will be avoided. This not only reduces costs, but the same boxes can be recycled more than once in a single year, reducing nominal yearly consumption of OCC.

At the same time, the US may be focusing more on domestic production instead of importing all its consumer goods—even more so with the new US president promoting domestic manufacturing and purchasing. This will lead to higher use of do-mestic boxes in the US, and most likely higher linerboard and medium production, as well as a higher share of OCC in the furnish. It also means less OCC available for exports, fewer imports of goods from Asia, and fewer empty containers available for cheap transport of OCC back into Asia. This has been a major competitive advantage for Chinese mills.

OCC AND OTHER GRADES

Newspapers and magazines are rapidly declining across the world, and office papers are not growing either. These have been an important source of recovered paper for recycled cartonboard producers. In the future, some of these volumes will need to be substituted by OCC, adding to the competition. Liner, medium, and corrugated box consumption is still growing rapidly in Asia, so more volume becomes available every year for collection. However, the population is aging, especially in the more developed countries such as Japan, South Korea, and Singapore, but also in China, Hong Kong, and Taiwan. An older population tends to consume less. However, family sizes are getting smaller and that means more packaging. Also, online shopping is growing rapidly in Asia, again helping to underpin consumption growth.

At the same time, the paper industry is growing in other fiber-poor regions, such as the Middle East and Africa. They need to develop their collection systems to meet the demand, but it is likely that they will also increasingly take part in the global OCC market. In the US, Europe, and Japan, box consumption grows slowly, so more needs to be collected from the existing volume. There is still room for the collection rate in the US to increase; however, additional tons will be more difficult to collect and the material will be lower quality and less clean with more impurities and other papers mixed in. Transport costs will also go up. The easiest tons have already been collected from big megastores like Walmart and Costco where clean boxes are collected daily and baled immediately. When you go to small towns and households to get the last remaining tons, it quickly gets expensive, and the boxes have often been reused or stored in poor conditions. In Japan, South Korea, and most of Europe, collection rates are already high, so very little more can be collected.

Single stream collection is increasing because it is a cheaper way to collect waste. This will support the growing trend in waste-to-energy, where plastic mixed with paper only adds to the heat value. This will limit the availability of OCC, especially more marginal household and rural volumes.

As a result of all these developments, the long-term trend price of OCC has been going up for the past 20 years already, and it will continue to rise. There will be short-term declines due to economic developments, new mills or closures that affect the regional balance. But the overall trend will be up. Higher prices will lead to more closures, but also to efficiency improvements, mergers, and maybe even new investments closer to the source of OCC, such as in the US.

The world is not going to run out of OCC. Yet when consumption grows faster than supply, it implies shortage and the price will increase, reducing demand. This will bring the world into temporary balance again, at a higher price level—and then the cycle will start again.