Understanding the EUDR: Challenges and Opportunities for the Forest Products Sector

RESOURCEWISE

Navigating the intricate landscape of global trade regulations, a new law can create significant disruptions, prompting businesses to swiftly adapt. The proposed European Union Deforestation Regulation (EUDR) is set to reverberate across the forest products industry. With the sector at the forefront and many stakeholders apprehensive about meeting compliance standards, it’s crucial to evaluate how the EUDR could transform the industry. Understanding how companies can prepare, adapt, and even thrive in response will be vital in the coming months.

KEY REQUIREMENTS AND RAMIFICATIONS

As global awareness of sustainability issues grows, the demand for greater transparency and accountability in supply chains intensifies. The EUDR is a response to this demand, mandating rigorous due diligence for commodities like timber and palm oil. These standards apply to nearly all solid wood products and most pulp and paper products, aiming to prevent the import or export of goods that contribute to deforestation or degradation of primary forests. The EUDR requires operators to provide:

- A due diligence statement attesting to compliance with the law.

- Geo-location data for every harvest tract that produced the wood or wood fiber in the product.

Non-compliant companies will face significant repercussions. These will include a prohibition on selling into the EU and fines of at least four percent of their total revenue earned from sales to Europe in the previous year.

By enforcing these requirements, the EUDR sets a new benchmark for environmental responsibility in business practices. The regulation places the onus on importers and exporters, referred to as “operators” in the legislation, to ensure their goods meet these stringent standards. Scheduled to take effect on December 30, 2024, for larger operators and June 30, 2025, for small- and medium-sized operators, the EUDR aligns with the core principles of the European Green Deal (EGD) and related policies. These policies leverage assertive trade strategies to achieve climate change objectives outlined in the Green Deal and the Paris Agreement.

In addition, the EUDR complements other EU decarbonization-driven trade policies, such as biofuel blending mandates (the “Fit for 55” package), the Renewable Energy Directive (RED II), and the Carbon Border Adjustment Mechanism (CBAM) for energy-intensive imports. Given its alignment with these climate change goals, ResourceWise believes that, while the implementation could face delays, it is unlikely to be abandoned.

CHARTING IMPACT AND IDENTIFYING VIABLE ROUTES

The forest products industry produces a wide array of end products, and the impact of the EUDR will vary across different segments. Certain segments will be more affected than others. For instance, pulp and paper producers who own and operate their own tree plantations for pulp fiber may find themselves at an advantage compared to those who source wood fiber from complex supply chains, which include forest thinnings, sawmill residual chips and sawdust, and harvest residues (tops, branches, etc.).

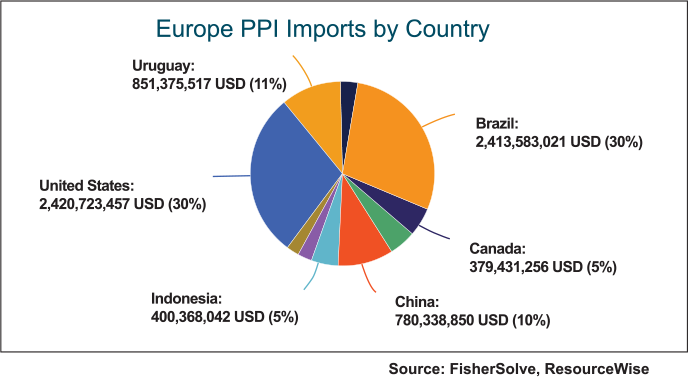

The pulp, paper, pellet, and solid wood industries collectively contribute billions of dollars annually to the EU economy. Non-compliance with the EUDR could jeopardize significant portions of these revenues, impacting not only individual companies, but also the broader economic landscape. Europe imports a substantial portion of its pulp and paper products from the US, the world’s largest pulp and paper exporter, with Brazil being a close second (see Fig. 1). Any loss or reduction in this export value would have far-reaching consequences throughout the industry.

According to ResourceWise, other forest product sectors exposed to EUDR impacts include wood pellets and hardwood lumber. Together, these three sectors—pulp and paper, wood pellets, and hardwood lumber—have an estimated US$4–5 billion of export value at risk (see Fig. 2).

SHIFTING DYNAMICS AND ECONOMIC IMPLICATIONS

The rapid growth rate of trees in the US South has traditionally attracted multinational companies to the region, thanks to its abundant supply of wood raw materials. However, the introduction of the EUDR, along with the Renewable Fuel Standard (RFSII) and RED III requirements, are beginning to alter this dynamic. Companies considering expansion into the US may now view the region’s lack of supply chain transparency as a significant barrier. If they cannot sell their US-manufactured goods in European markets due to insufficient due diligence documentation, they will likely invest in other regions where such systems are already in place.

The potential supply chain disruptions and revenue losses from European markets highlight the economic stakes of non-compliance. Beyond immediate financial impacts, failure to meet the regulation’s requirements could result in penalties and limit opportunities for tapping into new sources of demand.

Traders and producers in countries with higher rates of deforestation or weaker forestry management practices may find themselves particularly disadvantaged. The realignment of trade flows and the potential pressure on pricing and margins are additional challenges that companies must anticipate and strategize around to remain competitive.

ADDRESSING CONCERNS AND PREPARING FOR THE EUDR

Despite its ambitious goals, the EUDR has faced criticism and raised concerns among forestry professionals, companies, and associations. Critics have highlighted issues surrounding its scope, feasibility of compliance, and potential for international trade disputes. Nevertheless, the impending implementation of the EUDR demands close attention from all stakeholders in the forest products industry. The EUDR is not an isolated measure; it is part of a broader agenda toward a greener economy. This broader perspective suggests that companies aligning with the EU’s sustainability objectives could gain more than just compliance benefits.

However, there is growing concern about the practicality of meeting these regulatory requirements. Many organizations are advocating for potential amendments to the legislation or an extension of the enforcement date to address these challenges. For example, Austria’s forestry minister has called for EU states with no deforestation risk to be exempt from the regulation. Similarly, the US Senate has urged the US Trade Representative to engage with the European Commission regarding the challenges posed by the EUDR, stating that the regulation “poses significant concerns for our country.”

Navigating the complex web of EUDR requirements and market shifts necessitates a proactive stance. Despite the challenges and uncertainties, companies must develop a compliance strategy well in advance of the EUDR’s enforcement.

ResourceWise provides data, analytics, and consulting services for a robust range of natural-resource-based commodity industries, including forest products, low-carbon feedstocks and fuels, and chemicals. Learn more at resourcewise.com.